Ofgem have shared their Q1-24 view of domestic energy debt, reporting a total debt value of £3.3bn in the industry (54% increase since Q1-23).

Although the number of customers in debt has fallen for the second quarter in a row, total debt is the highest it's ever been, and average debt balances continue to spiral with a third consecutive quarterly increase of 10%.

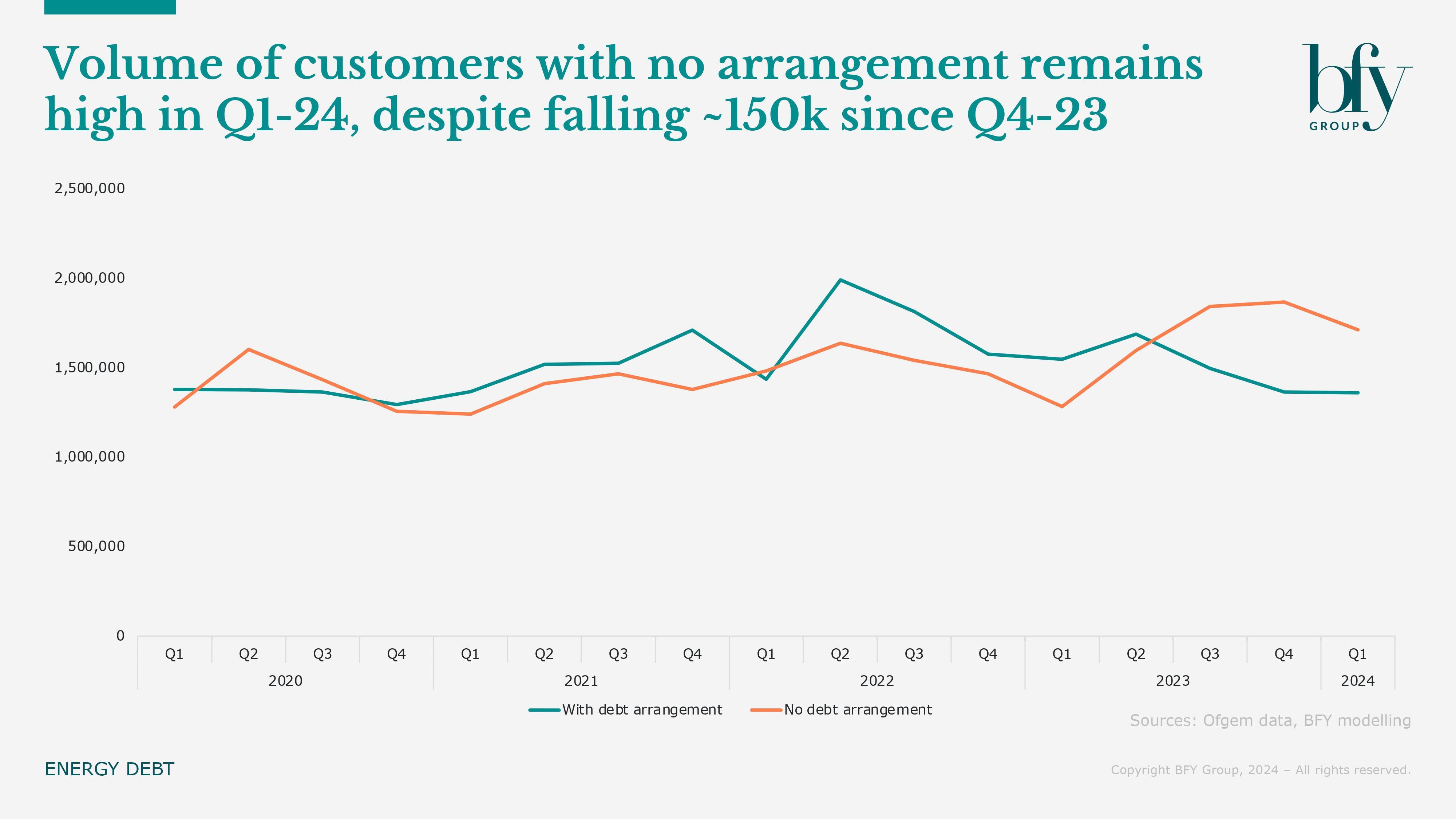

Energy suppliers need to be doing more to support customers without a payment arrangement in place, as they now make up 73% of the outstanding debt amount.

Internally, the focus should be on driving engagement and offering tailored debt solutions based on customer needs, while lobbying externally for the move towards a Social Tariff sooner rather than later.

The headlines remain striking:

- Average debt balances are now £1,052, up 42% year-on-year

- Number of customers with an arrangement is down 188k (12%) to 1.36m year on year

- Total number of customers with no arrangement are up 34% year-on-year, with average balances also rising 25% to £1,370 in the same period

Average customer debt balances keep rising – reaching £1,052 in Q1-24

We see a 240k (8.6%) increase in the number of customers in debt year-on-year, and despite annual bill price reducing since last quarter, the average debt balance as a % of price has increased in Q1-24 - continuing the upward trend seen since Q1-23.

The government’s £400 Energy Bills Support Scheme (EBSS) ended in March 23, and average debt has increased by £311 since then, despite annual price only increasing by £165. It means we're seeing the fall out of the EBSS disappearing and prices not falling, exacerbating the debt challenges faced by customers.

Ofgem are encouraging suppliers to act quickly to establish debt repayment arrangements, but have raised concerns about average debt levels increasing faster than inflation and the cost of energy in the past year.

Year |

Quarter |

Annual Bill Price |

Avg. Customer Debt Balance |

Avg. Debt as % of Last 12 Month Bills |

2023 |

Q1 |

£1,858.19 |

£741 |

39.9% |

Q2 |

£1,991.56 |

£793 |

39.8% |

|

Q3 |

£2,030.37 |

£873 |

43.0% |

|

Q4 |

£2,040.52 |

£960 |

47.0% |

|

2024 |

Q1 |

£2,023.44 |

£1,052 |

52.0% |

Source: Ofgem data, BFY modelling

Customer engagement and tailored arrangements remain key for suppliers

Whilst the new government is now in place, with a promise to save families hundreds of pounds and slash fuel poverty through GB Energy, change won’t happen overnight, and we expect the industry’s debt position will continue to worsen in 2024.

Suppliers need to hold the mirror up and satisfy themselves that they’ve tried all routes for engagement, offering non-standard arrangements where appropriate, to match the needs of customers with transient financial vulnerabilities.

We’re seeing cheaper products available to customers, but the debt problem isn’t going away, so it's a bigger issue than just the price of energy. It's the behaviours of customers, with increases in other household costs leading to more de-prioritisation of energy bills, meaning niche engagement is needed to provide help and support.

Key questions for suppliers include:

- Is the reporting and controls for payment arrangements in your business in a healthy place, with clear customer outcome tracking centred around stickability?

- Are your teams empowered to make in the moment decisions, to alleviate a challenging situation for a customer?

For more on how you can support customers in debt, through engagement and tailored arrangements, contact Rachel Littlewood.

Rachel Littlewood

Director

Rachel leads our operational and financial turnaround engagements, helping to solve complex operational challenges while maximising commercial performance and customer outcomes.

View Profile