The landscape of the retail energy market has undergone a significant transformation.

Retail energy suppliers no longer solely focus on commodity offerings, providing electricity and gas to consumers, but have instead started to shift towards service-oriented business models.

With these models being geared mostly towards renewables, the shift in market direction is here to stay, but how far suppliers should embrace it today is open to debate. An overriding risk is the size of the customer base for these diversified products – is it sizeable enough to generate a return on investment?

This question is creating uncertainty in the market, particularly for smaller suppliers, but there are opportunities across the board to make diversification a success. The key lies in customer engagement, and we’ve looked at how this can be leveraged to minimise risk and enhance margins below.

Trigger for change: Declining margins in commodity offerings

Since the introduction of the price cap, supplier pricing has been restricted. During the energy crisis, energy prices rose to the point where suppliers struggled to make a profit under the price cap. Today, the EBIT allowance is only 1.9%, significantly restraining margins for suppliers unless they can outperform other allowances.

Recent falls in the headline price cap have been welcome news, but suppliers are feeling a different type of uncertainty from Ofgem’s ongoing review of the price cap, which we covered here. These changes could further impact profitability:

- Standing Charge Removal: This will change the distribution of customers in hardship e.g., vulnerable customers with inefficient homes who are high consuming will be negatively impacted, resulting in an increased debt risk for suppliers.

- Operating Cost Allowance Review: There’s potential for operational cost allowances to be tightened, pushing suppliers to find further savings in commodity.

We’re slowly starting to see the market reopen, which comes with increased price sensitivity, as suppliers offer some fixed rate tariffs below the price cap, increasing competition. If this continues, increased customer switching could lead to suppliers investing in their margins to lower their price and so attract customers, further squeezing commodity margins.

The change: Suppliers are looking beyond commodity to drive higher margins

With the margins in commodity potentially declining further, suppliers have been on the hunt to source new revenue streams.

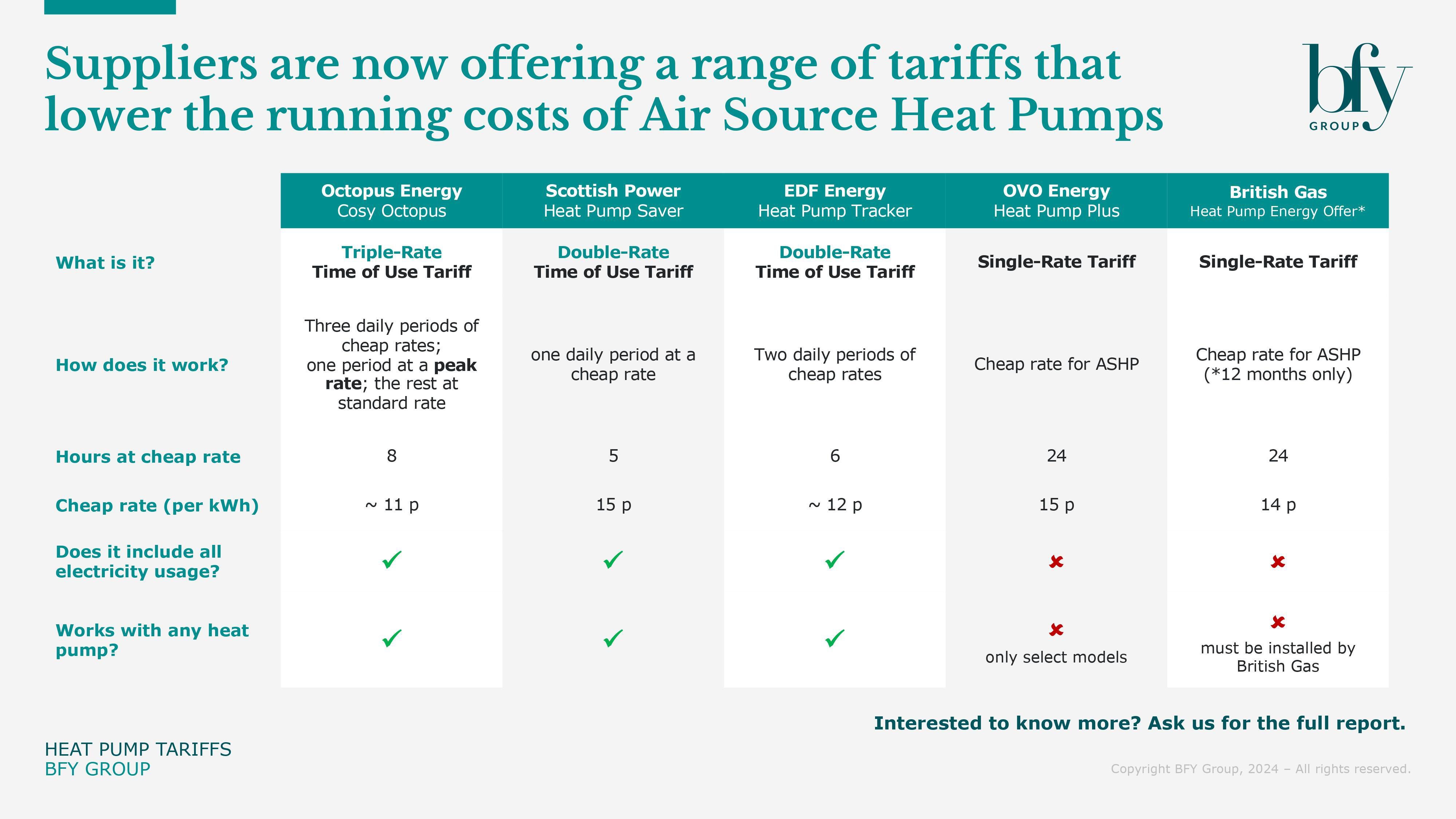

All major suppliers now offer renewable products such as air source heat pumps (ASHPs), solar panels, and batteries. British Gas is leveraging existing infrastructure to enable ASHP installation and servicing, whilst others like OVO Energy are forming partnerships with specialised companies like HeatGeek. Octopus have gone a step further, developing an in-house heat pump with a corresponding tariff to optimise usage, showcasing their commitment to net zero and this revenue stream.

Many have also embraced the transition to electric vehicles, with all major suppliers offering EV charge point installations and EV tariffs. Some suppliers have taken this to the next level. EDF have partnered with DriveElectric to offer car lease deals in conjunction with their EV tariff, whilst E.ON Next have partnered with Zoom EV to provide expert advice and benefits.

In addition to this, some companies have positioned themselves as energy saving experts, acting as a consultancy service on top of their commodity offering. OVO are offering the opportunity to have experts review home efficiency, and provide recommendations on how to improve it.

Diversifying product offerings not only stabilises revenue but also strengthens customer relationships and loyalty, making it harder for customers to leave, which is becoming increasingly important as the market re-opens.

Risk: Is the customer base for these diversified products big enough?

The success of diversified products hinges on customer uptake. High costs hinder the widespread adoption of heat pumps and EVs, despite government support, and The National Grid’s Future Energy Scenarios anticipate slow growth for both these markets.

In 2023, 36,799 heat pumps were installed, a far cry from the 600k annual installation by 2028 target. Additionally, the Government has already pushed back the target of 100% zero-emission new car sales from 2030 to 2035. The limited immediate growth of these products and the pushbacks of Government targets raises the question – has the diversification into these product offerings come at the right time?

Suppliers may follow in Octopus’ footsteps and develop their own in-house heat pump. However, due to tight commodity margins and the significant investment required, the current return on investment may be too limited to justify this.

The likelihood of both the heat pump and EV market becoming sizeable in the long term is variable and dependent on consumer engagement, however, what is clear is that these markets are not going to be sizeable for another 3+ years.

The high investment in these markets also comes at a risk for smaller suppliers. Larger suppliers are creating innovative tariffs and expanding their product offerings, potentially outcompeting smaller suppliers who may lack the resources to match these propositions.

Suppliers who are able diversify their product range also run the risk of being exposed to non-energy competitors in the market. For example, car manufacturers provide EV charge points and technology companies are offering home energy storage solutions, with Tesla creating the Powerwall home battery to support their electrified product offering.

Potential solution: Increased customer engagement

Diversification is a fantastic tool to protect profits, build stronger relationships with customers, and drive additional value. However, many of the products outlined above require significant investment which may not be available to all suppliers.

For those that have access to these product offerings, an evaluation of the current product performance across different customer segments will provide a clearer view of which customers to target, optimising take up of these products.

Suppliers could innovate customer interactions, leading to more tailored solutions like smart home integrations, informed energy monitoring, and personalised tariffs. Initiatives like Utilita Extra rewards could expand across multiple products, boosting engagement and satisfaction.

Through this innovation, suppliers should educate their customers on the benefits of these products. If customers are not aware of the product or the value that it brings, then uptake will be low regardless of the level of investment.

For suppliers lacking investment funds, alternative diversification strategies exist. Utility Warehouse, for example, offers a diversified product range without relying on energy-saving assets by bundling energy with broadband and mobile services.

To successfully diversify and increase margins amid tight operating costs and restricted revenues, energy companies should:

- Assess the market: is there a sizeable demand for potential products?

- Assess your funds: do you have the investment funds available to generate a sufficient return on investment?

- Assess your current customer base: what product offerings would they be interested in?

Diversification, if done strategically, can be the key to sustaining profitability and growth in the evolving energy market.

For more guidance on how to diversify effectively, and the impact of customer engagement, contact Tom Bromwich or Matt Turner.