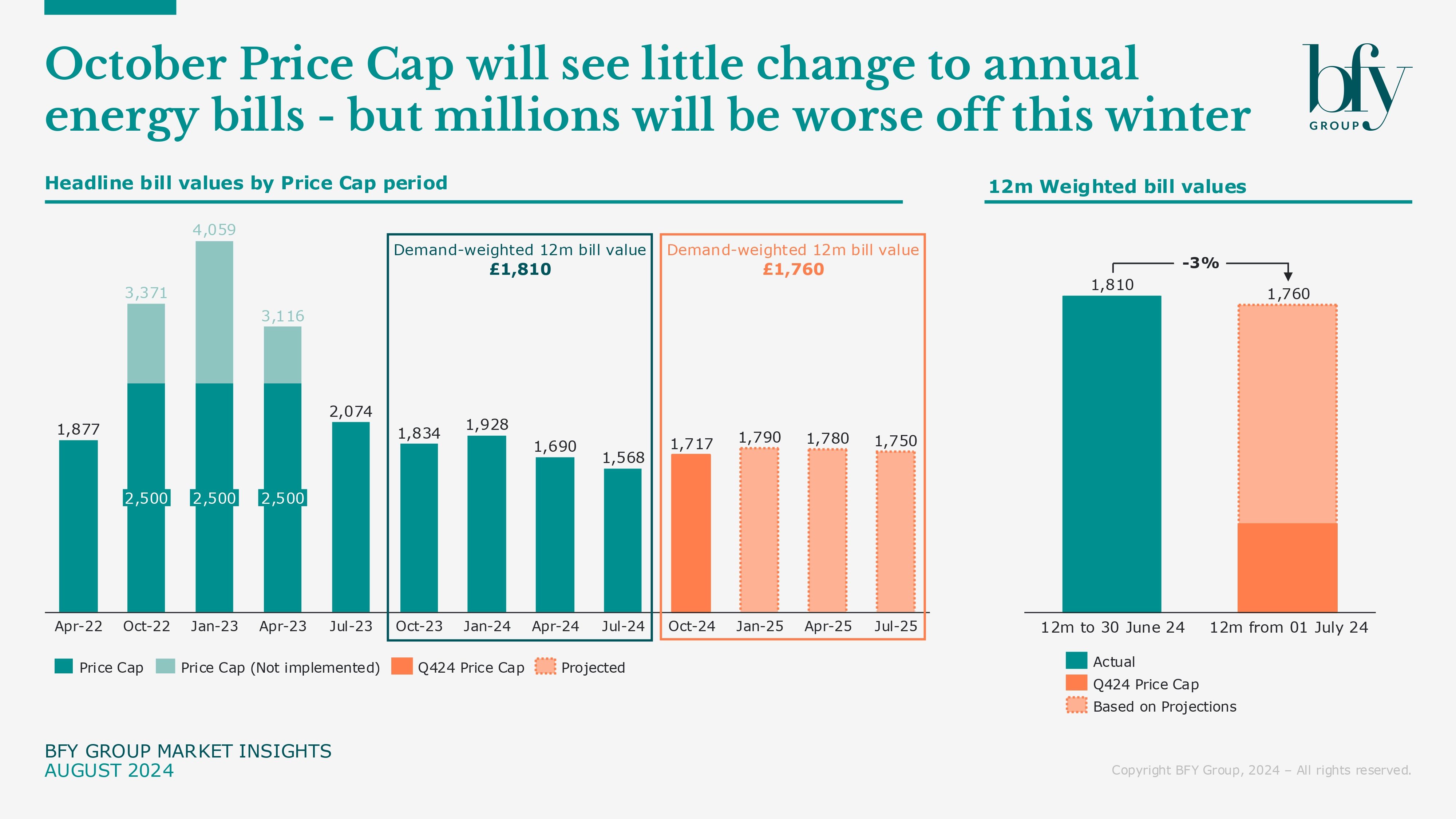

Ofgem have today (23 Aug) announced a 10% increase (£149) in the headline Price Cap, which will rise to £1,717 for a typical Direct Debit (DD) customer from October. It’s the highest level since Q1-24, and follows two consecutive falls.

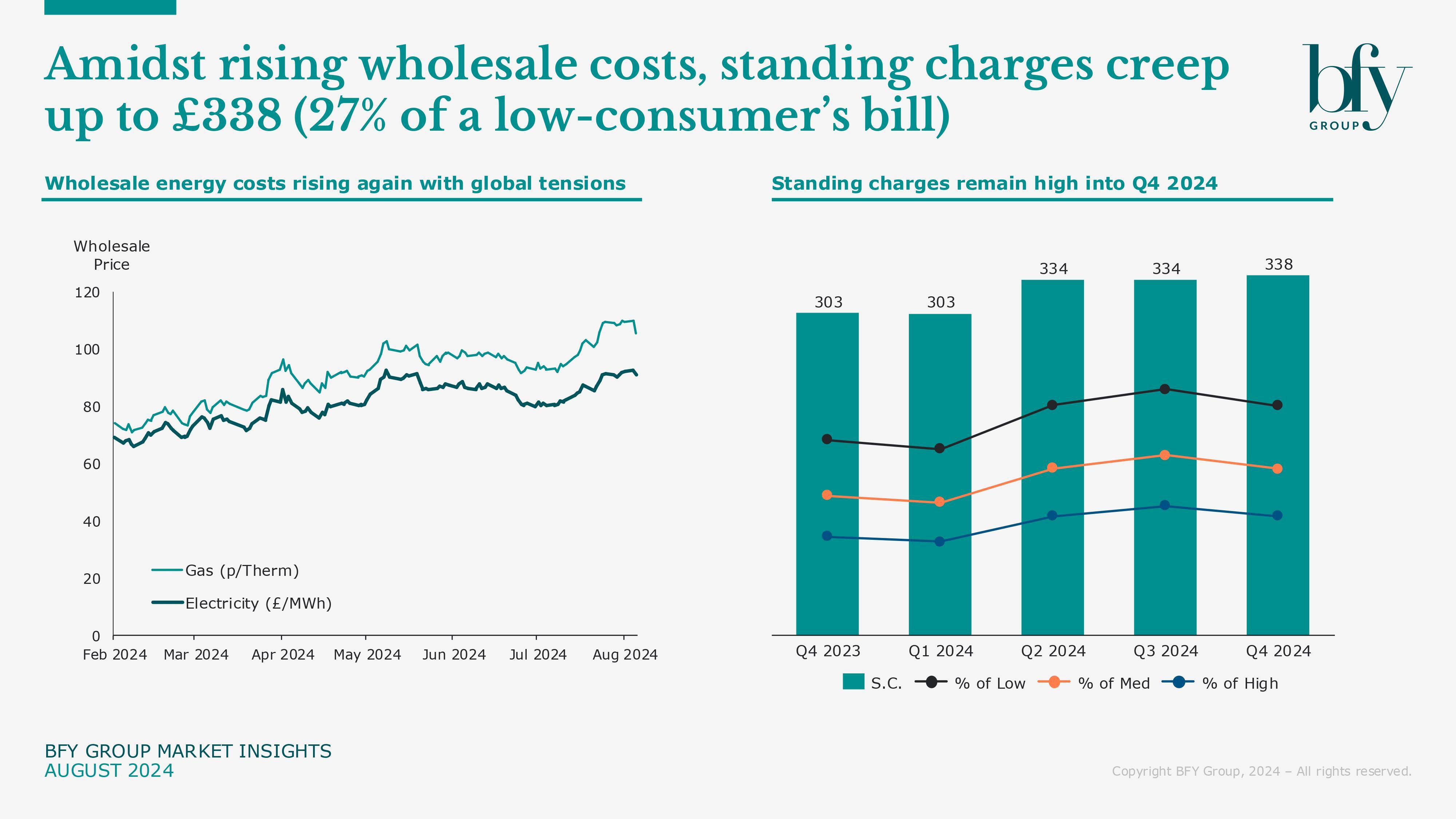

Today’s increase in the Price Cap is due to rising wholesale costs - an ongoing trend since February. We’ve seen renewed volatility, with global tensions contributing to a 15% increase in wholesale prices over the past 30 days.

Current wholesale prices suggest we could see further Price Cap increases in 2025, rising to ~£1790 in Q1-25. However, when adjusting average 12 month bills to reflect seasonal consumption, annual customer spending looks set to remain stable, which brings positives for customers and suppliers.

Levelisation between payment methods means this will be the first winter where prepayment customers see the lowest overall rates — however unlike Direct Debit customers, they face the challenge of paying winter energy costs upfront.

Average annual bills to remain stable – Is now the time to fix your tariff?

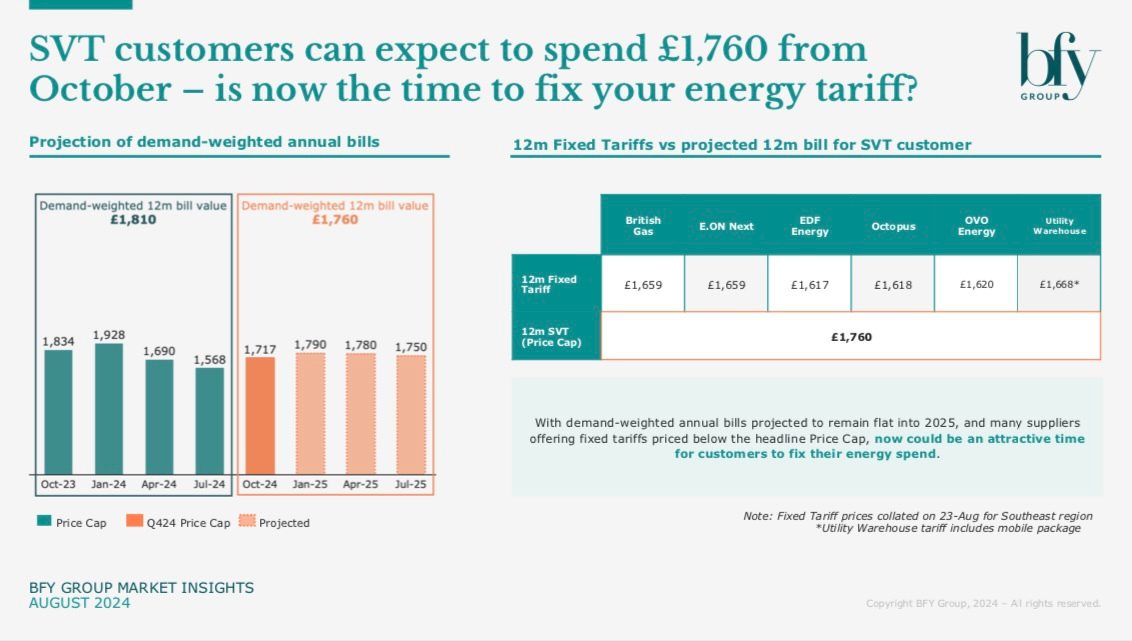

Based on our demand-weighted projections, we currently expect customers to spend £1,760 in the 12 months from 1st October. This is a fall of 3% (£50) compared to the previous 12 months. Although the lower prices seen in July’s Price Cap were welcome, they’ll have little effect on annual customer bills, due to lower seasonal consumption in the summer.

With annual bills projected to remain flat into 2025, and many suppliers offering fixed tariffs priced below the headline Price Cap, now could be an attractive time for customers to fix their energy tariff.

When comparing 12m fixed tariffs available today (23-Aug) with the projected 12m bill for an SVT customer (from 1st October), customers could save up to ~£150 over the year. This is based on one region in the UK, and some fixed tariffs may be available to new customers only, or as part of a bundle.

Regardless of whether customers choose to fix, stability in annual spending should make DD adequacy calculations easier for suppliers, enabling more accurate payment levels to be set, and providing a better experience for the majority of customers. Our modelling suggests typical DD payments should have stabilised this year, after a turbulent 2023 which saw DD failures rise sharply.

However, it remains essential for suppliers to ensure their messaging is reflective of the reality for customers. The headline Price Cap can be confusing, and rising prices going into winter will cause some anxiety, and potentially increased contact rates.

Millions of households worse off due to Winter Fuel Payment restrictions

Pensioners are set to lose out on £1.4 billion in support, as the government plan to restrict the Winter Fuel Payment to only those in receipt of pension credit. It means around 6 million households will be ~£200 worse off this winter (up to £300 in some cases).

Although use of the Winter Fuel Payment is unrestricted, it’s widely accepted that most of this money is spent as intended on energy bills. Losing the payment could have a material impact on households’ ability to pay these bills, especially for the estimated 2 million at risk of fuel poverty (including those who just miss out on, or don’t claim pension credit).

It’s particularly concerning for those households with lower consumption—who are most impacted by standing charges (which have risen to £338 per year).

Changes to the Winter Fuel Payment will create more pressure for suppliers, who now need to identify the impacted customers and provide heightened support throughout winter, while facing higher contact rates and record levels of customer debt.

When will we see changes to standing charges?

Labour have promised savings for customers by reducing standing charges. This follows Ofgem initiating a review of standing charges last year, issuing a call for input on their impact, and how costs could be fairly allocated across different groups of customers.

Today, alongside the Price Cap announcement, Ofgem published an Options Paper, continuing this discussion. The paper outlines possible changes Ofgem are considering, with a view to solving the affordability and debt challenges posed by standing charges on some customers.

To solve these issues, they’re considering two main courses of action:

1. Moving Operating Costs from standing charge to unit rate

Ofgem are considering moving a portion of operating costs, which currently make up ~40% of the dual fuel standing charge, to the unit rate.

Ofgem’s analysis shows this change wouldn’t impact suppliers equally, driven largely by their average consumption levels. Suppliers with below-average consumption could see a material impact to their EBIT, falling by 1.7% to 0.9%. Suppliers with above-average consumption would see their EBIT increase to 3.3%.

2. Driving diversity in tariffs

Ofgem see a problem with the lack of diversity in standing charges offered by suppliers. They’re considering ways to increase the number of low or no standing charge tariffs available to customers, including potentially mandating this.

Although not discussed in depth, one possible option is rising block tariffs, an idea which has been gaining traction recently.

Rising block tariffs could see the removal of standing charges, and a unit rate which rises progressively with consumption. This pricing structure could lessen the impact of suppliers’ fixed costs on households with low-to-medium consumption, potentially reducing bills for the majority of customers.

An advantage of rising block tariffs is that it could incentivise all customers to reduce consumption. As with all such schemes, there will be winners and losers, and provisions would be needed to ensure vulnerable households (e.g., those with medical equipment, or electrical heating) are protected from higher rates.

Ofgem recognise that suppliers alone cannot drive this change (each with differing business models and customer bases), and any sustainable solution will require major changes to the Price Cap mechanisms as we go forward.

Following today’s Price Cap announcement, Ian Barker (Managing Partner at BFY Group) said:

“Annual bills of over £1,700 will not be welcome for many customers - but there are fixed deals available now which could save households over £150.

We’ve been projecting bills of around £1700 for many months, which should also give customers some stability in Direct Debit levels.

Supporting customers remains a high priority, with customer debt already exceeding £3.3bn and likely to rise further. Cuts to the Winter Fuel Payment will also prove challenging for some customers.

We created our site PriceCap.energy to help customers understand the Price Cap and their Direct Debit levels, which many have taken advantage of this year.”

For more on the impact of October’s Price Cap increase, or how to navigate the commercial impacts of Ofgem’s consultations, contact Tom Bromwich.

Tom Bromwich

Director

Tom leads client engagements with a particular focus on commercial strategy, pricing, customer acquisition and retention.

View Profile