Recent media coverage is recycling something that as an industry we’ve understood for a while – energy debt is still going up. But why?

Compared to 2 years ago the macro economic picture is positive – prices have fallen significantly and incomes are outpacing inflation. This should all be driving debt down, but it’s growing. Our current understanding of energy is no longer explaining the trends we’re seeing so we need to start looking at this differently if we’re going to change customer outcomes.

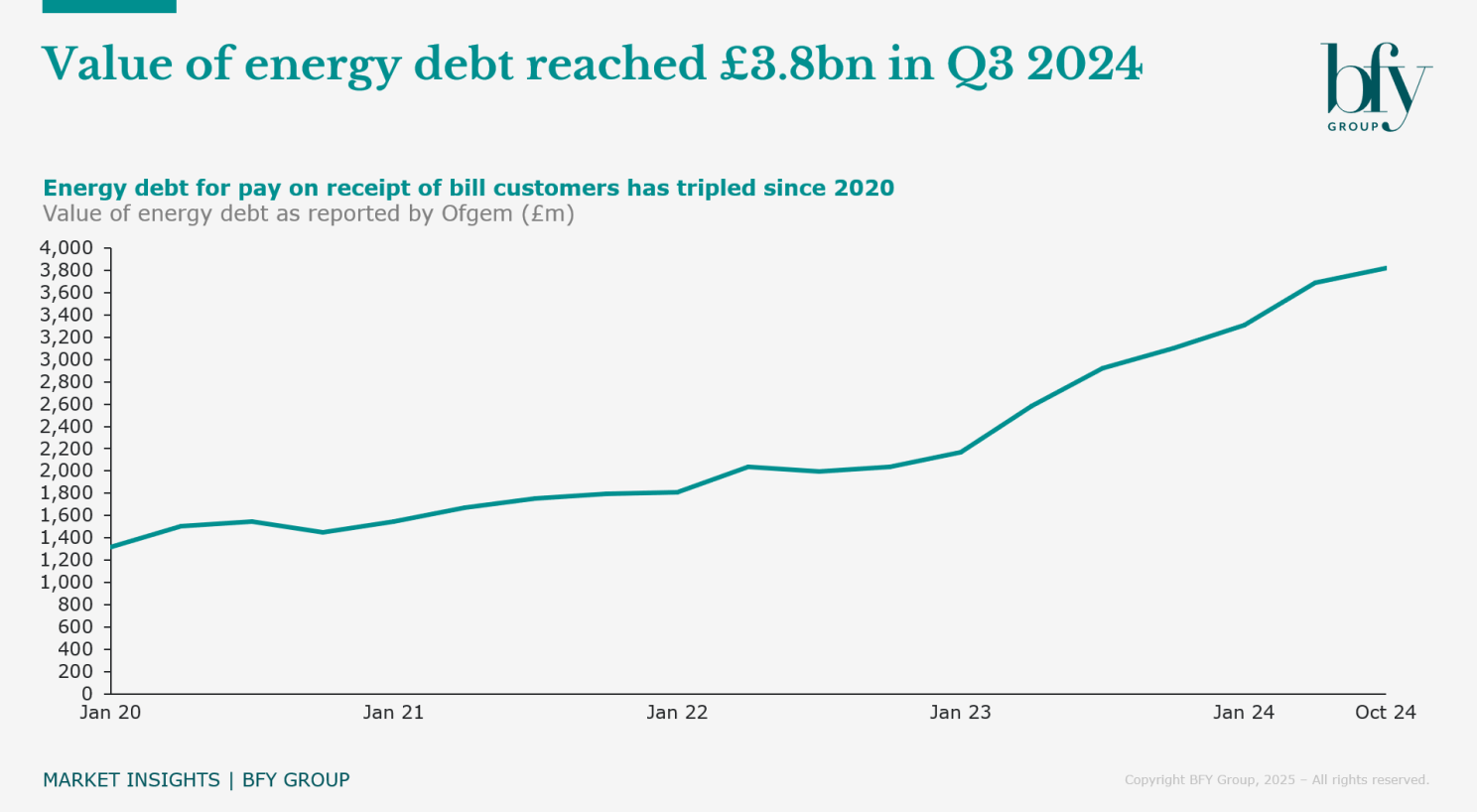

Energy debt has been rising since 2018, but it accelerated in 2020 to £1.5bn and spiked sharply from 2022, growing 163% to hit £3.8bn by Q3 2024, according to Ofgem. However, this figure only represents debt from customers paying on receipt of bill (less than 20% of households) and those with arrears over 91 days. Ofgem doesn’t currently publish this data, which supresses the scale of the issue.

Source: Ofgem data

Energy prices and the general cost of living have long been seen as obvious drivers of energy debt. However, while total debt balances are beginning to stabilise, the number of customers in debt - as defined by Ofgem - is rising (up 6% since Dec 23), despite the ~30% reduction in bills we’ve seen since 2022.

This matters deeply for customers who need help to improve their financial situation, but it also matters for the wider industry which is now focussed on the energy transition and net zero. This will only be possible in partnership with energy consumers, requiring customers’ engagement in the market. Achieving net zero through customer engagement in the market is incompatible with customers continuing to wrestle with this level of debt and unaffordability.

What’s driving energy debt, if not energy prices and cost of living?

The answer may lie with the 70% of households paying by Direct Debit (DD). Fixed Monthly DDs are an energy industry phenomenon that aim to predict the customers’ bill for the year ahead and split it into 12 equal payments, removing seasonality. In theory, whilst your balance will fluctuate throughout the year, by your anniversary it should have balanced out and have you back at a zero balance, starting the next year with a clean slate. In a stable market this works well, but with the volatility we’ve seen in the last 5 years the fixed DD system has been put under significant pressure.

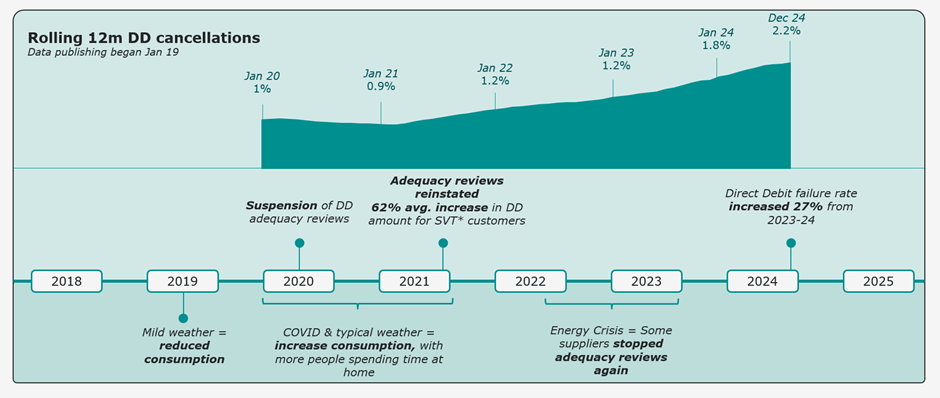

Analysis of ONS and BFY data seems to reflect this pressure, showing that DD defaults are still rising, long after energy prices have dropped. The average failure rate in 2024 was 2.2%, up 27% on 2023. These defaults are also diverging from previously correlating trends seen in other sectors, like mortgages and water, suggesting there’s something unique happening in the energy sector. The concern is that energy debt and payment defaults has passed a tipping point and we’re now in a compounding loop of DD failures.

Source: BFY Group analysis of ONS and Ofgem data

While the broader cost of living crisis has certainly affected energy customers’ finances, our analysis suggests that there is no longer a direct and simple link between price increases and DD failures, meaning something else is driving the rise in defaults.

We can also see that this isn’t a new trend. The data shows a steady increase in DD failures since April 2021, towards the end of the pandemic. The rate of growth increased slightly during 2023 and then slowed slightly but 2024 still saw a 27% YOY increase in the DD failure rate.

It’s plausible therefore that the beginning of this rise in DD failures can be traced back to the suspension of payment adequacy checks during the pandemic. In response to government measures in 2020, many suppliers paused DD reviews to ease customers' financial pressure during lockdown.

Whilst well intentioned, this likely crystallised many customers’ DD payments at a level far too low to cover their consumption. The winter of 19/20 was unusually mild (average temperature 5.3°C), reducing the typical energy consumption being reflected in DDs. However, winter 20/21 (average temperature 3.5°C) was more seasonally normal, leading to higher consumptions year on year. This was then compounded by a further increase in consumption throughout 2020 driven by lockdown (12% for electricity, 9% for gas). This means heading into 21/22, many customers would have fallen into arrears, likely leading to sharp increases in DD payments once reviews were reinstated.

We have evidence of this in 2022 when Ofgem revealed that customers on standard variable tariffs saw an average 62% increase in their DDs in Q1, with 10% facing hikes over 100%. In comparison, the price cap only rose by around 50%. This led to enforcement action from the regulator and a social media campaign encouraging customers to stop paying, leading to a small but noticeable spike in DD failures.

As a one off, this situation could probably have been recovered eventually as things began to normalise, with any future dip in prices offsetting the balances, putting most customers back in a neutral position. Unfortunately, this didn’t happen as later in 2022 the energy crisis kicked in and suppliers once again took the decision to pause DD reviews.

By the point DD reviews were fully restarted in 2023 some customers had been underpaying their energy bills for over 3 years. We don’t know exactly what was owed at that point in time as the data has never been published. However, with a conservative estimate of a 20% underpayment each year, average balances could have been close to £1000.

Faced with significant deficits, suppliers then increased monthly payments to recover these debts. As repayments rose to cover the debt, defaults also increased, creating a vicious cycle of higher repayments and more failures.

DD failures as a time series against market conditions and responses

Despite falling prices, this cycle has persisted, and it’s hard to see it ending without a change in approach. It’s worth noting that suppliers do have policies limiting the number of failed payment arrangements, but in my experience, these are often poorly executed and monitored. This is largely because advisors genuinely want to help customers and given a choice between having a risky DD in place or leaving them to pay on receipt of bill and likely disengage completely, it seems like an easy choice in the moment, even if it isn’t the right long term answer.

We can see this behaviour playing out in the data too. Despite a rising percentage of payments failing, the number of customers paying by DD has actually increased 1% throughout 2024 according to DESNZ.

This also explains the growing balances and propensity to be in debt of customers paying on receipt of bill. Eventually people will drop out of this loop – whether that’s customers finally giving up or suppliers’ refusing any further arrangements.

This itself has broader consequences. Only 3% of receipt of bill customers are currently on fixed tariffs (flat on last year) compared to 20% pre-energy crisis and 25% pre-pandemic. Fixed tariffs are seen as a barometer for customers’ engagement with the energy market. While this link was broken for a while with the energy price guarantee making price cap the cheapest tariff choice, DD customers seem to be returning with 19% now on fixed tariffs compared to 13% last year. As well as signalling increasing disengagement from receipt of bill customers, this trend also leaves them far more exposed to price fluctuations, which now come quarterly within the price cap mechanism.

Source: DESNZ

With a different understanding, how can we address the issue?

Now that we better understand the challenges, we’re able to think more in a more targeted and intentional way about solutions.

To break the cycle, we need to ensure that monthly payments are truly affordable at an individual customer level. The two levers for this are the amount being charged for consumption, and the amount being recovered for arrears.

There are three main groups of customers failing DDs, each requiring different support:

- Those who can afford their consumption and some debt repayment, but not at the level their supplier is asking for.

- Those who can afford their consumption but no debt repayment.

- Those who can't afford their consumption.

Group 1

The most pragmatic solution is to make debt repayments more manageable. This can be done by extending the repayment term, similar to those seen on prepayment meters. The standard policy for the maximum length of debt repayments on DD is 12 months. Longer arrangements are possible, but they’re the exception, and as with all exceptions, the approach to them can be inconsistent. Offering schemes like matched payments where the supplier contributes to the arrears whilst the customer is making payments could also help. Small-scale trials have shown success here, but we haven’t seen large-scale deployment yet.

Critically these payment arrangements must be carefully monitored throughout their term. They should be excluded from automated checks and flagged for manual review when prices rise to maintain stability. Rigour is key but in my experience it’s these controls that are often missing, rather than the availability of these arrangements in the first place and without them customers will find themselves back at square one. Although this approach may seem antithetical for the areas of suppliers focused on the commercial impacts of customer debt, it will lead to better outcomes than letting customers fall into a cycle of failed payments and growing unsustainable debt that will ultimately be written off.

Group 2

Bolder actions are required for this cohort. Ofgem's debt relief scheme, which is currently in consultation and exploring writing off debts for customers who stay current with future payments, may be helpful, though its design and targeting are critical. Additionally, grants from suppliers’ hardship funds could help here, though likely not at a scale that solves the full problem. Emphasis for this group should be on long-term financial recovery, and the evidence to date shows mixed outcomes for customers receiving these grants with some suppliers seeing success rates of just 50%. I would suggest this is down to issues in targeting and understanding whether the customer being supported is the right one.

Group 3

Even more significant interventions are needed for these customers who are often the most financially vulnerable with many experiencing true fuel poverty. This is an issue that sadly continues to grow and is interlinked with social issues like poor housing and health problems. Energy suppliers alone cannot solve this; joined up central policy is essential and should focus both on the affordability of energy for this group, but also enhanced data sharing to improve identification of these customers.

While discussions about social tariffs, bill discounting, and other interventions are ongoing, no actionable solutions have emerged yet. In the meantime, debt collection efforts from suppliers are likely wasted, and resources would be better spent supporting those with more sustainable outcomes. This isn’t to say these customers should be ignored; regular contact will maintain engagement and make sure changes in circumstances are recognised quickly, individual customer based approaches aren’t likely to resolve the problem.

All Groups

At a strategic level suppliers should also be aiming to move customers from cohort 3 to cohort 2, and from cohort 2 to cohort 1, eventually reducing the need for ongoing support. By reducing consumption, more funds are available for debt repayment. Targeting energy efficiency measures will help. Partnering with financial charities can offer budgeting advice, help customers prioritise spending, and ensure they’re accessing all available benefits to increase their income. Ensuring these customers are on the best tariff is also important. While it may seem like a zero sum game for suppliers, it can significantly help customers by enabling them to reduce debt and regain financial control.

Affordability cohorts and options for support

How do we prevent this reoccurring in the future?

In terms of prevention, many of the same solutions apply. Arrangements need to be truly affordable. A nationwide solution to fuel poverty needs to be in place.

But also we must learn from our past well-intentioned interventions during crises and understand their long-term impacts. Knowing what we know now, would we still have made the decisions to stop payment adequacy reviews? How do we assess the future impact of these decisions? Does a fixed payment for an increasingly variably priced product make sense?

To help us work through this, full transparency of industry debt is essential for market transformation. Long-term price affordability and stability are now widely believed to only be possible in the event of a successful energy transition. However, this cannot succeed without the support of customers and the current debt crisis is breaking trust and driving more customers to disengage entirely.

Contact Rachel Littlewood for more on how we can help with customer debt.

Rachel Littlewood

Director

Rachel leads our operational and financial turnaround engagements, helping to solve complex operational challenges while maximising commercial performance and customer outcomes.

View Profile