Despite energy prices falling and incomes outpacing inflation over the past two years, customer debt continues to grow, reaching £3.8bn in Q3 2024. New analysis from Rachel Littlewood at BFY Group challenges the traditional understanding of debt in the industry, highlighting systemic issues in the way customer payments are managed.

Key points:

- Traditional understanding of debt is failing: Energy debt has risen despite a 30% reduction in bills since 2022 and incomes outpacing inflation. Total debt balances are beginning to stabilise, but the number of customers in debt is up by 6% since December 2023.

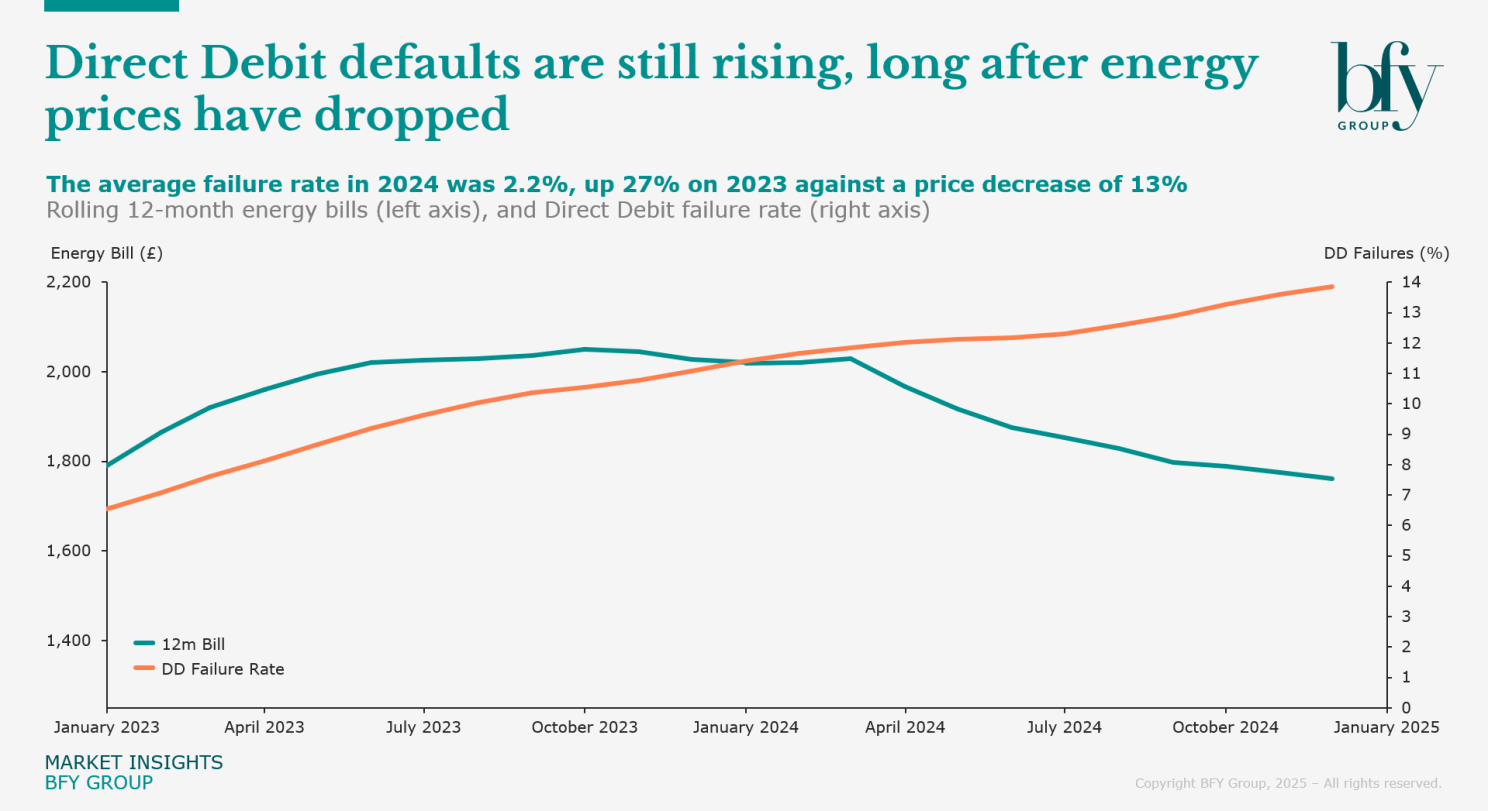

- Direct Debit system is creating a failure loop: Payment default rates rose by 27% year-on-year to 2.2% in 2024, even as energy prices dropped. This trend contrasts with other sectors like mortgages and water; raising the concern that debt and defaults are beyond a tipping point, creating a loop of failures.

- No direct link between prices and DD failures: While cost-of-living pressures have impacted customer finances, price increases alone no longer explain Direct Debit failures, pointing to deeper structural issues.

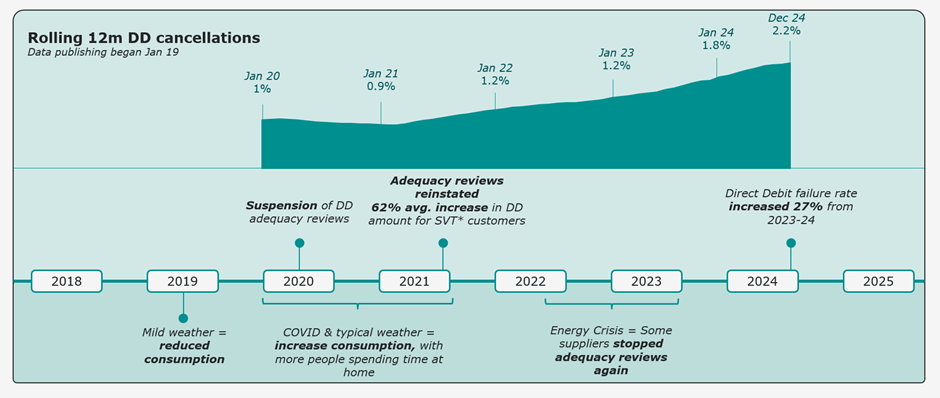

- Rise in DD failures traces back to pandemic: Suspended payment adequacy checks during the COVID pandemic led to prolonged underpayment. When reviews resumed in 2023, some customers had been underpaying for over three years, leading to estimated balances of ~£1000. With suppliers increasing monthly payments to recover this, defaults also increased – a vicious cycle.

- Solutions needed to prevent persistent failure cycle: Default and debt cycles will continue without an industry-wide shift. Supplier policies to limit failed payments are often poorly executed and monitored, as advisors typically prioritise keeping risky Direct Debits over potentially disengaging a customer. However, without sustainable payment solutions, this approach only prolongs the issue.

Understanding the true drivers of energy debt

The Direct Debit (DD) system, used by 70% of households, was designed to smooth out annual energy costs but has struggled with market volatility. BFY Group's analysis identifies long-term structural flaws, driving a cycle of DD failures and rising debt.

"Our analysis shows that energy debt is no longer simply a function of high prices or cost-of-living pressures," said Rachel Littlewood at BFY Group. "We're seeing a compounding cycle of debt driven by systemic issues in how we manage customer payments, particularly through the Direct Debit system."

Energy debt has been rising since 2018, but it accelerated in 2020 to £1.5bn and spiked sharply from 2022, growing 163% to hit £3.8bn by Q3 2024, according to Ofgem. However, this figure only represents debt from customers paying on receipt of bill (less than 20% of households) and those with arrears over 91 days. Ofgem doesn’t currently publish this data, which supresses the scale of the issue.

Analysis of ONS and BFY data seems to reflect this pressure, showing that DD defaults are still rising, long after energy prices have dropped. The average failure rate in 2024 was 2.2%, up 27% on 2023.

BFY analysis suggests that the rise in DD failures can be traced back to the suspension of payment adequacy checks during the pandemic. In 2020, many suppliers paused DD reviews to ease financial pressure, unintentionally locking customers into payments that were too low to cover their actual energy consumption.

Mild weather in winter 2019/20 led to artificially low DD levels, but a return to normal temperatures in 2020/21, combined with lockdown-driven energy usage increases (12% for electricity, 9% for gas), pushed many customers into arrears. By the time reviews resumed, significant underpayments had accumulated.

In early 2022, Ofgem reported that some customers saw DD increases of over 100%, even though the price cap had risen by only 50%. This sparked enforcement action and consumer backlash, leading to a spike in DD failures.

Instead of recovering, the crisis deepened as suppliers again paused reviews during the 2022 energy crisis. When reviews fully restarted in 2023, some customers had been underpaying for over three years, with estimated average debts of nearly £1,000. The sharp repayment increases triggered a cycle of defaults and mounting arrears - one that continues to drive today’s growing energy debt crisis.

The cycle of failed payments and mounting energy debt continues, even as prices fall - highlighting the need for a new industry approach. While suppliers have policies to limit failed payment arrangements, poor execution and monitoring often undermine their effectiveness. Advisors, aiming to support customers, frequently maintain risky DDs rather than risk full disengagement, despite long-term consequences.

This pattern is evident in the data. Despite rising DD failures, the percentage of customers paying this way has increased by 1% in 2024, according to DESNZ. Meanwhile, customers paying on receipt of bill are accumulating larger debts, with many eventually forced to drop out of the system entirely.

A key indicator of disengagement is the decline in fixed tariff uptake. Just 3% of receipt of bill customers are now on fixed deals - unchanged from last year but drastically lower than the 25% pre-pandemic. By contrast, DD customers are returning to fixed tariffs, with 19% now on deals compared to 13% last year. This growing gap leaves receipt of bill customers more vulnerable to price volatility, reinforcing financial instability in an already fragile market.

Targeted solutions needed to break the energy debt cycle

A new understanding of the energy debt crisis allows for a more strategic and tailored approach to tackling the issue. Rather than a one-size-fits-all solution, different customer groups require specific interventions to ensure payments are manageable and sustainable.

Three key customer groups facing Direct Debit failures:

- Customers who can afford consumption and partial debt repayment – but not at the level their supplier demands.

- Customers who can afford consumption but not debt repayment.

- Customers who cannot afford their energy consumption at all.

Tailored support for meaningful change

For Group 1, extending repayment terms beyond the standard 12 months and introducing matched payment schemes.- where suppliers contribute to arrears as customers make payments - can make debt recovery more manageable. Rigorous monitoring is essential to prevent customers from falling back into unsustainable debt cycles.

For Group 2, bolder action is required. Ofgem’s proposed debt relief scheme could provide critical support, alongside better-targeted supplier hardship funds. However, effective targeting is key to ensuring these interventions lead to long-term financial stability.

For Group 3, deeper interventions are necessary. Many in this group experience fuel poverty and broader financial struggles, requiring a joined-up central policy approach. Enhanced data sharing would improve identification, while discussions on social tariffs and bill discounts need to move toward actionable solutions.

A long-term vision for sustainability

Beyond immediate relief, energy suppliers should aim to transition customers up the ladder - from crisis to stability -by reducing consumption, improving energy efficiency, and ensuring access to tariffs. Partnering with financial charities to provide budgeting support and benefits advice can further empower customers to regain financial control.

Without industry-wide reform and targeted intervention, the energy debt crisis will continue to grow - impacting not only customers but the wider energy market as well.

How do we prevent this reoccurring in the future?

To prevent recurring debt cycles, payment arrangements must be truly affordable, and a nationwide fuel poverty strategy is essential. The industry must also assess the long-term impact of crisis-driven interventions and rethink the suitability of fixed payment models for a fluctuating market.

In addition, lessons must be learned from past interventions. Knowing what we know now, would stopping payment adequacy reviews have been the right decision? How do we better assess the future impact of similar policies? More fundamentally, does a fixed payment system still make sense for an increasingly variable-priced product?

Full transparency on industry debt is critical for market reform. Long-term price affordability and stability are widely believed to be achievable only through a successful energy transition. However, this cannot happen without customer trust and engagement. The current debt crisis is breaking that trust, driving more customers to disengage entirely, and jeopardising the long-term sustainability of the energy sector.

"Full transparency on industry debt is essential for market transformation," added Littlewood. "Energy transition and price stability depend on customer trust and engagement, but unsustainable debt levels are eroding both. Without urgent action, we risk prolonged financial distress and stalled progress toward net-zero goals."

About BFY Group

BFY Group is one of the UK’s fastest-growing management consultancies, trusted by leading energy and utilities organisations, as well as investors supporting the sector.

We build strong partnerships with our clients, working practically to tackle their toughest challenges, realise opportunities, and achieve lasting results. Our deep expertise is what sets us apart. We bring in leading talent directly from the sectors we serve, equipping them with the consulting skills they need to make a lasting impact with our clients.

BFY Group is recognised as one of the UK’s Leading Management Consultants by the Financial Times, receiving five awards in 2025. We’re featured in The Sunday Times Hundred as one of the fastest-growing private companies, and have earned multiple Great Place To Work awards. Our Private Equity clients also voted us as one of the 50 Most Ambitious businesses and leadership teams in the UK.

For PR and media enquiries, contact: pressoffice@bfygroup.co.uk